Expo West 2026 trends (and why they matter)

+ this bidet company wants you to eat fiber, a spammy collab, and more

Welcome to our first post-Expo newsletter (1 of 2). If you’re already over all the Expo talk, scroll down for our regular news roundup. If you’re waiting to learn about our favorite bites/sips, you’ll want to check out Friday’s send. Today, we’re diving into the themes. It’s gonna be a good one.

This was an incredible show, and while an ode to our wonderful community is certainly in order, we’ll save the sappiness for LinkedIn and cut to the good stuff: the themes that defined this year’s show.

Let’s get into it →

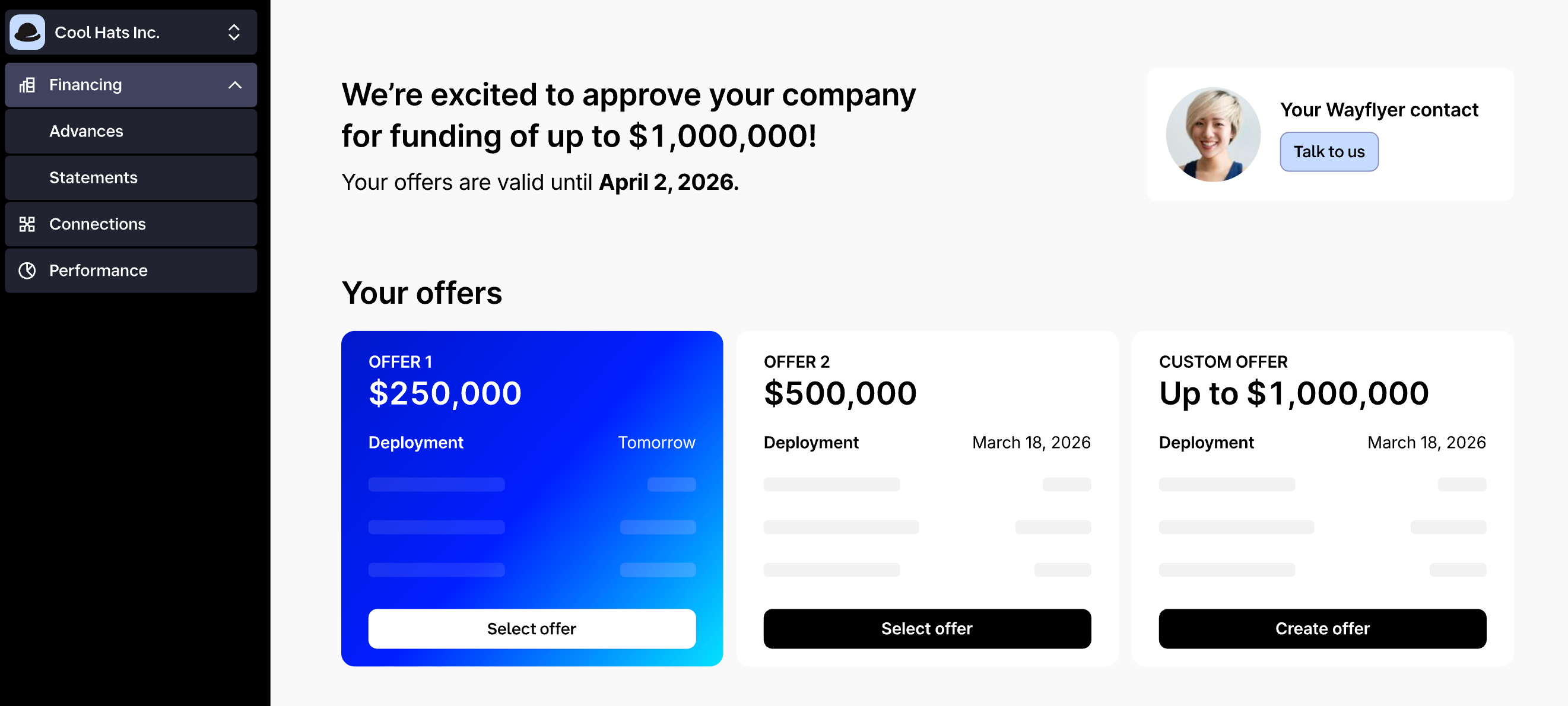

Wayflyer showed up to Expo West with $1 billion to deploy!!

Did you spot the Wayflyer taxis darting around Anaheim? See their team scouting for great brands on the floor? Or maybe you grabbed a beer with them at our Network + Noms event?

They’re a non-dilutive financing partner to some of the hottest brands in CPG right now, deploying over $6 billion to 6,000+ brands so far, including many that were at Expo.

Matt from Big Mozz told us: “Once we got to 4,000 doors, we really needed to pour fuel on the fire. That’s when we started working with Wayflyer.”

If you didn’t get a chance to connect on the floor, it’s worth setting up a conversation with their team here!

Expo West 2026 Trends

After 72 hours, over 100,000 combined steps, many interviews at The Angel Group booth, a successful event at Bubba Gump Shrimp, and countless samples… we have successfully wrapped up our time at Expo West 2026!

The vibes. Expo West 2026 was, by most measures, a tamer show than we’ve seen in recent years—and that felt right.

Overall, the trends that showed up were exactly what you’d expect if you’ve been paying attention. In previous years, brands leaned more into niche ingredient or nutrtional callouts. But this year, there weren’t any major “jaw-dropping” or “eye-roll” moments on the show floor. Things felt dialed back and more sensible.

Even the politics were quieter. Last year’s show was unabashedly MAHA—booths, merch, fear-mongery copy and all. This year, brands were still making the same implicit arguments (see: every “no seed oils” callout), but without waving a flag about it. There was less telling, and more showing.

Brand collaborations were also notably scarce—whether because recent ones simply haven’t moved the needle, or because founders are now laser-focused on their own brand equity, it’s clear people are betting on themselves right now… not some trendy brand’s logo slapped on their packaging with a subtle nod to the brand’s flavor.

So why the vibe shift? We think it was mainly two things:

First, there was some real anti-Expo momentum leading up to the show—namely, founders writing LinkedIn posts about why the ROI doesn’t justify the cost. It seemed to work: the people who needed to be there were, and the ones who didn’t, weren’t.

But the bigger force is the funding environment. It’s been a forcing function for brands to get serious about profitability over the past year. Flashiness doesn’t cut it when you actually have to show your work.

With all that being said, here’s (some of) what we saw on the show floor. →

The Themes

Eggs. Like, literal eggs. It all started when we stumbled upon a jammy egg from Chino Valley Ranchers—the first packaged soft-boiled egg. We were excited to see this innovation (single-ingredient innovation is very of-the-moment), but we had no idea it was only the beginning of an incredibly eggy show.

The players: Oegg, Fearless Eggs, Kipster, Egglife

Why (we think) it’s happening: You could chalk it up to America’s current protein fixation (certainly a massive part of it), but we think there’s more here:

First, it’s a response to the recent egg shortages and price fluctuations that transformed eggs from an everyday item to something of a delicacy.

Secondly, consumers are getting increasingly concerned with where their eggs are coming from (see: Vital Farms’ recent scandal)

And finally, it’s not just about protein. It’s about protein quality. The 2026 protein fiend isn’t just interested in any protein—they’re looking at source. They’re growing skeptical over added protein and seeking whole food sources instead.

The new era of fats: beef tallow + avocado oil. It feels silly to say that there is always a Fat of the Moment, but there is. A few years ago, ghee had a huge moment with the rise of keto. Then there was coconut oil for its MCTs. Then olive oil came back in a big way (thanks, Graza). And now, we’ve landed on two new stars: beef tallow and avocado oil.

The players: Jesse & Ben’s, Steak & Shake, Masa/Vandy, Doughbrik’s Original Wavers (avocado oil), and many many more

Why (we think) it’s happening: Yes, this is about the demonization of seed oils. There’s no doubt about it: nearly all of the brands that called out beef tallow and avocado oil also called out “no seed oils.” But there must be something else here—olive oil, ghee, butter, and coconut oil are also not seed oils… but we aren’t seeing them show up in the same way.

Avocado oil won because it’s genuinely versatile, feels premium, and brands like Primal Kitchen made it the “clean” seed oil replacement for the wellness crowd.

Beef tallow won because the carnivore/ancestral diet community needed a hero fat, and the “McDonald’s used to use it” story gave it a perfect villain-redemption arc.

Protein and fiber, of course. Would you have expected anything less from a food and beverage trade show in 2026? While we did see plenty of big callouts and protein- and fiber-dedicated brands, there were plenty of brands who simply changed their packaging to call out the protein and fiber amounts they already had. Instead of protein and fiber “maxxing,” it was more toned down and treated as a dietary staple—moving from last year’s 40+g protein callouts, to products with just 5-7g protein still calling it out.

The players:

New protein or fiber-focused SKU launches: Hippeas tortilla chips and puffs, Sweet Lorens new Ready-to-Bake scones and oat bars, That’s It’s new fiber bars, Banza going beyond gluten-free with its new wheat protein pasta, Elmhurst moving from plant-based milks and creamers into RTD protein drink

Protein/fiber callouts: Meat sticks in great abundance (including Chomps new Chicken meat sticks), Wonder Monday’s new packaging emphasizing its existing high-protein

Truly an ungodly amount of meat sticks….look at how many Raquel here found! 👇

Why (we think) it’s happening: As protein and fiber saturate the mainstream conversation, consumers are becoming more educated on both. Now, they’re beginning to understand that more doesn’t always equal better, and are looking for products that combine protein + fiber, even if both are present in more modest amounts. If anything, consumers may associate those crazy double digit protein figures with less healthy, more processed products.

Pucker up, because sour is in! Spicy has had its run–and honestly, it’s not going anywhere–but sour is quickly pushing its way into the conversation. While spicy might have been all the rage, sour is quickly taking its throne. Sour candy challenge videos are up 81% on social media, and menu mentions of sour flavors have grown 15% in just the last two years. Beverage forecasters are already tracking “swour” (sweet and sour) as one of the defining flavor mashup evolutions of 2026. And that was very prevalent on the show floor.

The players: Built Sour, Pur gum’s new sour gum, Simply new sour mints, Goodpops sour pops, Joolies sour dates, and green apple flavored everything (Be Love and Ryl Ice Tea)

Why (we think) it’s happening: There are a few things leading up to this.

Social media. Sour, like spicy before it, has become a spectator sport. Who can consume the most sour snack and live to tell the tale? Just look at the growth of Final Boss Sour—the gaming-themed, real-fruit sour snack brand built in the Science Inc. studio (the same team behind Dollar Shave Club and Liquid Death). The brand has earned over 700 million organic views across TikTok, YouTube, and Instagram, and recently closed a $4M Seed 2 round.

The “Fruit Riot effect.” You can’t deny the wild impact this brand has had. It’s so simple, yet so fun, and people can’t seem to get enough of it.

Citric Acid is a cheat code. It’s cheap, versatile, and the moment you dust it on a date, a chip, or a gummy, you’ve got something that tastes like candy but still reads as “better for you.”

Dates are having a big moment. You absolutely could not escape dates during this show. This sweet, candy-like fruit is finally getting the attention it deserves—whether it’s highlighted as the base of a “natural” candy or used as a “natural” sweetener or key ingredient in sweets. Though its hard to imagine a world without this trend, dates weren’t always the “it girl.” U.S. searches for “Medjool dates,” hit a 20-year high in March 2025, and U.S. retail sales of dates jumped about 30 percent in the 52-week period ending in July 2025 compared with the year before.

The players:

We saw four (4) different brands turning dates into candy: True Dates (the OG), Joolies, Smood, and Daddl.

Harken and Freakin’ Wholesome are both candy brands that are sweetened with dates

Why (we think) it’s happening:

The low-GI angle resonates more now. Blood sugar management has become a mainstream wellness concept, not just a diabetic concern, and dates score well on GI relative to traditional candy.

The sugar villain narrative needed a hero. As consumers moved away from refined sugar and artificial sweeteners, they needed something that felt indulgent but “allowed.” Dates are sweet enough to feel like a treat, but they come wrapped in fiber, minerals, and a whole-food story. That’s a very easy sell to the wellness crowd.

Baking mixes are back, and they’re getting an upgrade. The humble baking mix—long live Betty Crocker and boxed brownies—is getting a premium makeover. What caught our attention wasn’t just the products, but who was launching them: brands with established culinary credibility moving into a new format, bringing both better ingredients and better taste to a category that hadn’t seen much innovation.

The players: Cravings by Chrissy Teigen (leaning into quality ingredients and a chef-driven sensibility), Seven Sundays (a clean cereal brand) launched its first pancake mix, Mochi Foods with mochi baking mixes, Nowhere Bakery expanding into at-home baking mixes

Why (we think) it’s happening:

The pandemic baking era never fully ended… it just got more discerning. Consumers who picked up baking habits in peak COVID are still baking, but they’ve developed opinions. They know what a good pancake tastes like now, and the original box isn’t cutting it.

The “restaurant effect” happening in CPG more broadly: consumers are bringing higher taste expectations home, and they want products that actually deliver on flavor, not just convenience.

For some of these brands (Seven Sundays, Nowhere), better ingredients are part of the story too. But across the board, the throughline is quality—whether that means cleaner labels, more interesting formats like mochi, or just a mix that produces something you’d actually want to eat.

Real dairy’s comeback. For years, the story in dairy was about alternatives—we’d come back from Expo reporting on “what else got ‘milked’ this year.” But this Expo felt different. While there were a ton of great plant-based milk alternatives present, we saw an equal counter-narrative emerging: brands doubling down on the real stuff, and leaning into provenance, fermentation, and specialty milks as the differentiators.

The players: Sourmilk (everyone’s new favorite gut-health-focused yogurt), Painterland Sisters (organic Skyr yogurt that leans into its family farm story), le zette (sheep’s milk products made in small batches in LA), Ice Cream For Bears, and obviously Chobani (which had the most incredible booth we’ve ever seen… footage to come!)

Why (we think) it’s happening:

The perfect combo of protein + gut health. Dairy is a natural protein source, and consumers are paying attention to that as they double down on protein source + quality. And just like how we mentioned that people are looking for protein with fiber, consumers are looking for protein with gut health benefits: fermented dairy products like kefir and sour milk sit at the intersection of the probiotic trend and the real-food trend, making them an easy win for ingredient-conscious consumers.

Plant-based dairy has had a rough few years, and real dairy is filling the credibility vacuum, especially when it comes with a farm story or a specialty milk type.

Global flavors aren’t going anywhere. They’re actually getting even more specific: what’s shifting now is brands moving from language like “Asian-inspired” to specific regional cuisines, ingredients, and techniques. This space isn’t saturated—the floor is just rising.

The players: Nomad Popcorn’s Pad Thai and Ramen flavored SKUs, Saffron Road’s new Crossroads line, Soom’s new squeezeable tahini SKUs in mediterranean flavors like Harissa, Hippeas’ new “All Dressed Up” puff SKU (a take on the UK’s famed chip flavor, All Dressed), and of course matcha being everywhere, notably Oatly’s upcoming launch of a new matcha RTD.

Why (we think) it’s happening:

Gen Z and millennial consumers grew up more culinarily adventurous than any prior generation, and their palates are demanding specificity. “Asian-inspired” doesn’t cut it anymore—we know the difference between Thai and Japanese, and want brands to know it too (preferably, want brands to know it personallytoo).

TikTok and IG continue to surface hyper-regional foods, and generally globalize flavor trends in an instant.

Disclaimer: This is not a comprehensive list. There was too much we wanted to cover! We shared a few different themes/trends on our Instagram, and we will be sharing even more on this week’s episode of The Curious Consumer (subscribe so you don’t miss it!), including more specific flavor trends, function trends, and some trend predictions based on our observations.

CPG & Consumer Goods

The year of the poop jokes. Tushy, known for its easy-to-install bidet system, just launched a once-daily prebiotic dietary fiber gummy under a separate brand name, Reboot Gummies (the perfect name, in our opinion).

Great way to increase your TAM as a bidet company? Get more folks to the toilet. Brilliant.

Tushy’s core customer is already someone who thinks about gut health, digestive wellness, and bathroom habits more consciously than the average consumer. Launching a fiber gummy is serving the same customer at an earlier point in the same journey: The bidet is the hardware, the gummy is the software.

It’s also such a smart LTV angle. A bidet is a one-time purchase, but a daily gummy is a subscription. If even a fraction of Tushy’s existing customer base converts to Reboot, they’ve created a meaningful recurring revenue stream off an audience they already own.

A match made in heaven. SPAM teamed up with Bachan’s to launch a limited-edition Japanese Barbecue Sauce flavored SPAM, which is now available at Walmart.

We love to see this kind of collaboration. Founder and CEO of Bachan’s, Justin Gill, grew up eating SPAM, and SPAM musubi has become a popular Japanese American fusion food.

It’s a great halo for both: SPAM gets a credibility bump from a beloved indie brand with serious food-world cachet. Bachan’s gets mass distribution exposure and association with a product that has genuine cultural roots in the communities Bachan’s was built to represent.

It’s world tour time. poppi, the better for you soda brand, is officially launching in the UK, introducing five flavors—Strawberry Lemon, Raspberry Rose, Lemon Lime, Wild Berry, and Orange. The brand aims to disrupt the soft drinks aisle with a low-sugar, high-fiber profile, available initially at Tesco and Pret A Manger.

Just last week, we talked about the opposite trend happening: a British invasion of CPG brands launching in the US. The US market produces brands at scale that can then export back. It’s a two-way street, and the brands winning on both ends are the ones with the resources and retail relationships to actually execute.

The UK is a smart first market. Better-for-you soda has real traction there—consumers are already primed by the sugar tax (introduced in 2018) to seek out low-sugar alternatives. The category infrastructure exists. And Tesco plus Pret is a smart channel combo: mainstream retail reach with a foodservice halo that puts the product in front of commuters and lunch crowds daily.

‘Tis the season of iced tea. Spindrift is entering the iced tea market with a new line, featuring real brewed tea and real squeezed fruit (no added sugar) in flavors like Lemon Black Tea and Peach Green Tea, available in 12oz cans.

Iced tea is increasingly added to the list of “I want something flavored, but not soda” drinks. The category is large, fragmented, and mostly owned by legacy brands that haven’t innovated meaningfully in years. Just Ice Tea’s recent $9M raise and now Spindrift’s entry both signal that better-for-you players see a real opening.

The brand built its entire identity on sparkling water made with real squeezed fruit. Brewed tea + real fruit is the same thesis, just still. It’s a natural extension that doesn’t require consumers to learn anything new about the brand—it just asks them to reach for it in a new occasion.

This will be Spindrift’s first product line with the full portfolio verified as Non-Ultraprocessed Food. We spoke with the Spindrift team about its Non-UPF verification here!

Hair care → body care. Amika, the hair care brand, is expanding into body care launching a three-piece body collection featuring a body wash, whipped body butter, and vitamin C body oil. This expansion is apparently in responds to strong consumer demand—97% of Amika users requested a body care line—and taps into prestige body care’s growth over the last year.

We’re seeing a broader trend of beauty brands expanding beyond face and hair into body care, while simultaneously bringing facial skincare ingredients—like vitamin C, peptides, hyaluronic acid, and ceramides—to the rest of the body. Brands like reflect this shift, as consumers increasingly seek comprehensive beauty routines with high-performance actives across all categories.

A little something for the boys. New men’s grooming brand Blvd & Co launched in 2,682 Walmart stores with shampoos, conditioners, and styling products affordably priced around $10.

What makes Blvd & Co smart is its approach: the branding is clean and still traditionally masculine without being alienating, and the pricing is very accessible. Since men often don’t buy grooming products for themselves, keeping prices at parity with what they’re already used to should help drive trial and adoption.

Men’s grooming is so ripe for disruption. U.S. men’s grooming sales topped $7.1 billion in 2025, up nearly7% year over year, and yet the category has barely scratched the surface of what’s possible.

With overall beauty sales showing signs of stabilizing after five years of explosive growth, brands and retailers are turning to men to sustain momentum. Target partnered with streaming collective AMP to launch TONE, a men-forward personal care brand that debuted in stores nationwide in July, leaning into the platform’s massive Gen Z male following. Walmart is taking bets on brands like Blvd & Co.

Plus, there are some cultural tailwinds playing into this space. Gen Z men are the biggest spenders in the male beauty category, with 42% saying they devote a larger share of income to grooming, and men ages 18-24 were twice as likely to shop at Sephora in 2024 than in 2020.

eCommerce

There’s an over-discounting epidemic going on. Sounds counterintuitive, right? Tapcart’s 2026 Mobile Trend Report interviewed 1,200+ shoppers and found that 50% of shoppers only need 25% off to convert, yet brands are still bleeding margin at 40-50%. We’re all for a good deal... but this margin leak is simply unsustainable for emerging brands.

Turns out, there are far better incentives for shoppers, like BOGO (the #1 most motivating promo for 2026) which drives value for customers wanting to stock up.

If you’re an ecomm brand, check out this report for strategies (including plug-and-plan Ai workflows you can implement instantly) from leading brands like Reformation, Gymshark, and Cymbiotika.

Retail

Private label takes on “restaurant quality.” Kroger is expanding its Private Selection brand with over 20 new fresh and frozen meals featuring global flavors, including “Korean Inspired” Beef Bulgogi and “Gnocchi Alla Sorrentina.”

Premiumization and global flavors are big in the frozen aisle. Brands like Wildgrain, Laoban, Mason Dixie, Ripi, and more are redefining what frozen food means, and giving retailers and private label brands something to respond to.

This is also probably a direct response to Target, which expanded (and seriously premiumized) its private-label frozen brands to include chef collaborations including frozen pizzas and apps from James Beard Award-winning chef and restauranteur Ann Kim.

Funding news

Leaning into hydration. After raising a $2 million seed round, our friends at Pricklee pivoted from “cactus water” to a “natural hydration” drink, aiming for national distribution and a stronger foothold in mainstream markets. Five years in business, it’s clear they’re ready to hydrate on a larger scale.

We saw their rebrand and got to try their new flavors IRL at Expo (spoiler: it’s SO tasty)! So proud to have known this brand for all five of its years in existence and to see it continue to grow into itself.

What’s most interesting here is their repositioning away from “cactus water.” Yes, “natural hydration” leans into an obvious trend, but this is more clarifying what the brand always had. Before, you had to explain what cactus water was, why it was good for you, and why someone should choose it over coconut water or plain water. “Natural hydration” sidesteps all of that and puts Pricklee in a much bigger, more intuitive category.

As Co-founder and CEO Kun Yang told us:

“Our mission has always been to help families build better hydration, naturally. Our repositioning as a Natural Hydration leader enables us to truly maximize the reach of that mission, by reducing ingredient-led education and focusing more on hydration, and approachable fruit flavors that families love.”

Crisp(y) new funding. Mezcla, the plant-based protein bar brand famous for its “puff crispy” texture, raised $9.5 million in a Series B funding round to bolster brand building and expand distribution. Mezcla also shared its newest flavor at Expo, Frosted Strawberry!

If you haven’t yet, please subscribe, like, leave a comment, and share it! It helps us continue to bring you the most interesting news + nuance in consumer and retail every week.