Big Food is officially obsessed with fiber.

+ an interview with OLIPOP's CEO, co-founder, and formulator

Hello hello!

To our northeast friends: hope you’re all staying warm and your surroundings have been well-shoveled! With just one week until Expo West (!!!!) we’re certainly ready to ship off to sunny CA. If you’re attending Expo, we’re so excited to see you there!

Curious what high-growth ambassador programs do differently?

They recruit. Consistently.

High-performing programs build predictable recruiting systems: Daily outbound, follow-ups, and active response handling. Often, teams spend hours every day keeping the pipeline active.

But the reality is, most brands don’t have that team. Consistency becomes the bottleneck.

Endlss’s Creator Recruiting Agent runs targeted, on-brand outbound aligned to your brand voice and alerts you when qualified creators engage.

It’s targeted, personalized, and structured—like having a recruiting team built in, without adding headcount.

Turn recruiting into a predictable growth lever.

News From the Week

This week, we’re doing something a little different… and launching our very first full interview series for The Curious Consumer podcast: Brand’s Biggest Fan! This has been a labor of love, and we cannot wait to hear what you think.

The premise: We sit down with a self-proclaimed “biggest fan” of some of our favorite buzzy CPG brands—not influencers or famous ambassadors, just regular people who happen to be a little obsessed with a brand.

Then, we go back to the founders of these brands to learn how this fandom aligns with—or departs from—the story they’ve told themselves about their own brand’s success. By kicking off the convo up with a consumer story, we open up a different kind of founder interview—one that spans far beyond the typical “brand story” interview.

We were SO fortunate to launch this series with the one and only Ben Goodwin, CEO, co-founder, and formulator of OLIPOP!

There are countless fantastic learnings and insights in this episode—from how Ben thinks about nostalgia when formulating OLIPOP, to soda’s wild history and what that means for consumer perception and so much more.

If you give it a listen, be sure to let us know what you think (hello@expresscheckout.co)! And if you just so happen to know (or be) a buzzy brand’s biggest fan, let us know—maybe we’ll feature you in our next episode.

Much more to come, so be sure to subscribe on your listening platform of choice so you never miss an episode.

CPG & Consumer Goods

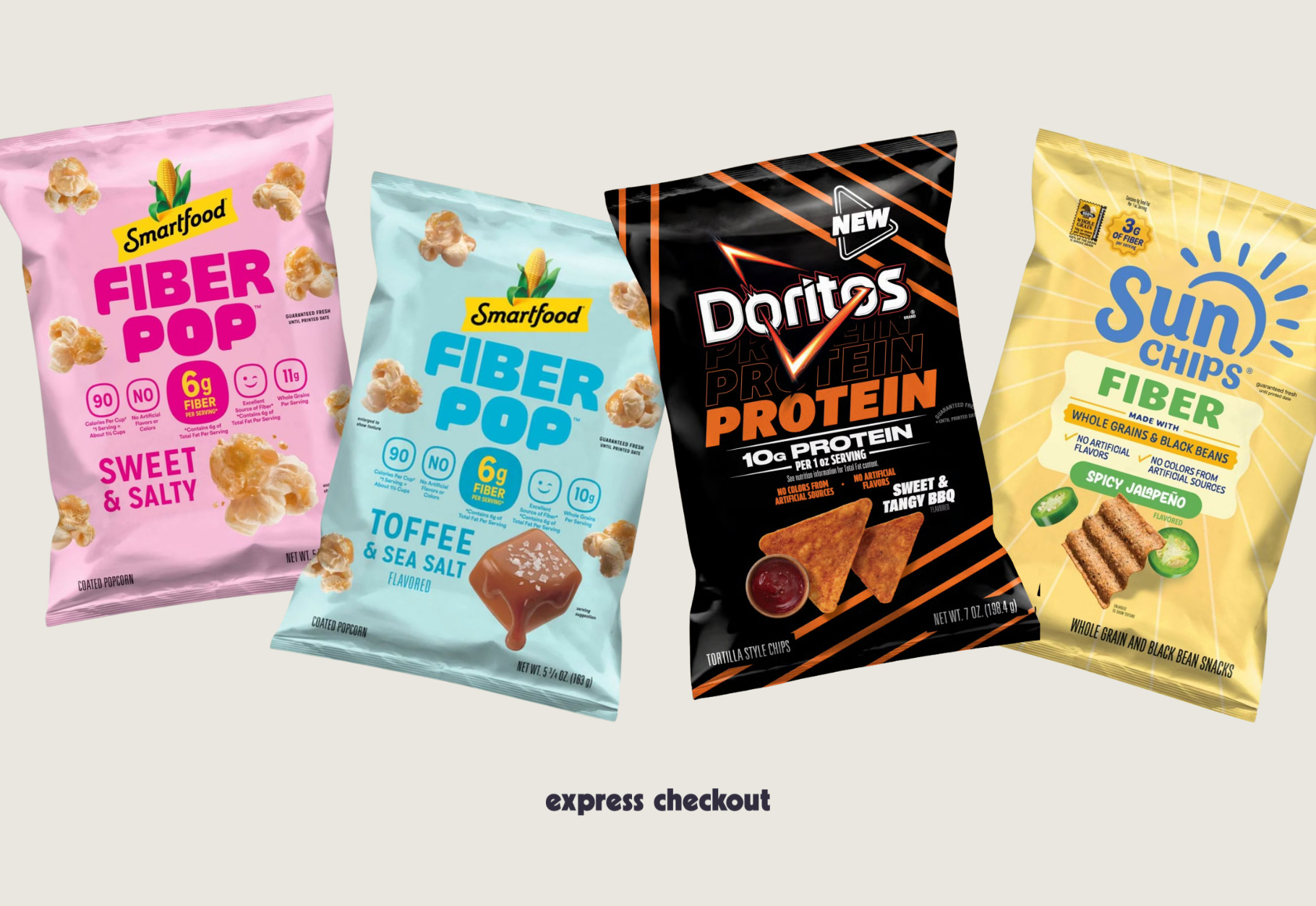

What happens when big brands hop on health trends? PepsiCo is certainly attempting to answer. At last week’s Consumer Analyst Group of New York (CAGNY) conference, PepsiCo announced its plans to capture the fiber and hydration trends (shocker)—highlighting whole grains in products like Quaker and innovating with Gatorade and Propel. The company will apparently focus on enhancing its offerings with lower sugar options and “clean-label” attributes across brands, while also expanding into crafted beverages and ready-to-eat meals.

We already saw some movement here in PepsiCo’s recent launches: A new fiber-rich Smartfood line, fiber-focused Sun Chips, and prebiotic sodas. At CAGNY, the brand also showcased Quaker’s new “Gut Support” granola bars and high fiber oatmeal.

And don’t think the behemoth forgot about the protein craze: Last week, PepsiCo also announced its launch of the new Protein Doritos, featuring 10g of protein per 150-calorie serving (7 servings per bag) with Milk Protein (casein) as its first ingredient… and vegetable oil as its second.

Something interesting happens when strategics like PepsiCo get in on the latest health trend: it both amplifies and dilutes the claims. With all of the funds in the world to conduct great consumer research, PepsiCo can confidently stake claim on what’s trending. But at the same time, when BigCos get their hands on a trend, consumers grow skeptical. There’s a meaningful difference between a brand built around gut health (like OLIPOP) and a brand that retrofits gut health onto an existing product line. Protein Doritos with vegetable oil as its second ingredient are not a health food, no matter where you stand on the seed oil debate.

That said, PepsiCo’s reach is genuinely unmatched. If Smartfood Fiber Pop ends up in every Target, Walmart, and CVS in America, more people will be eating more fiber—and that’s not nothing. Big CPG has always been better at scaling health trends than starting them. Emerging brands light the spark; the Pepsis of the world pour the gasoline.

The real question? Whether fiber will become a lasting priority for the big guys, or just this year’s fun new feature. Given that PepsiCo is buying its way into BFY (see: the $1.95B Poppi acquisition, the $1.2B Siete deal), it’s clearly putting its money where its mouth is. But consumers (and we) will be watching to see whether the follow-through translates meaningfully to the nutrition label… or just front-of-pack claims and marketing material.

In actual fiber + protein innovation news… Lasso, a new food tech company, just announced its commercial debut of its Lasso SpinTech process with two owned brands: Froobies and CronchClub.

For my fellow nerds 🤓: Lasso’s SpinTech is a proprietary tech that uses centrifugal force to create texture from protein and fiber. A less fancy way to put that? It’s basically a cotton candy machine, but instead of sugar, Lasso uses protein and fiber. The machine spins fast, which outputs tiny threads that weave together into a fibrous material that can then be shaped into snacks, fruit chews, meat alternatives… you name it.

This is a big deal because, typically, snacks achieve their texture from gums, binders, or artificial ingredients. In Lasso’s case, the spinning force naturally “glues” everything together, so nothing needs to be added.

As Lasso CEO Mike Messersmith shared, “Consumers want real innovation, not legacy brands repackaging familiar formulas with added protein and calling it progress,” (editor’s note: see above 🙃). “Today’s shoppers are more informed and expect meaningful improvements in ingredients, nutrition, and formulation, and they want it now.”

I got to try both Froobies and CronchClub at Winter FancyFaire, and was seriously impressed with both! Froobies is a fruit snack with 4g protein and 5g fiber per serving, without any added sugar or anything artificial, while CronchClub is a “baked crisp” (think: flavored cracker) with 21-23g protein and 7-8g fiber per serving. Both have the cutest branding—especially for brands that are essentially just commercial proof points for a food tech company. Look out for Lasso—I have a feeling they’ll play a role in developing some of the biggest snack brands or products in the coming years. - Jenna

Another gut(sy) lawsuit. Halfday Tonics faces a proposed class action lawsuit over its gut health claims, which tout “prebiotic benefits” despite containing only 6 grams of fiber per 12 oz. can—hardly enough to make a difference, according to the complaint.

This looks a lot like Poppi’s class-action lawsuit, which we cited in our recent article about “functionwashing.” But this time, the brand contains a lot more prebiotic fiber than Poppi—6 grams of a blend Cassava Root Fiber, Fructan Fiber, and Organic Agave Inulin.

We have yet to see the details of the lawsuit, but I’m a bit confused about the basis of this claim. Unlike Poppi’s measy 2-3g of prebiotic fiber per can, Halfday’s contain 6g—which does fall within the effective daily dose of 5-10g. On top of that, Halfday’s fiber blend approach is actually quite aligned with where the research is headed (towards fiber source diversity). From my understanding, it’d be hard to find peer-reviewed support for the idea that 6g of a multi-fiber prebiotic blend is clinically inert, but I’m no lawyer… - Jenna

Moon Juice comes to Target. Moon Juice is making a bold entrance into mass retail, landing in 755 Target stores nationwide with a focused lineup of magnesium products, including a $43.99 Magnesi-Om 30-serving jar and two flavors of Magnesi-Om stick packs (~$25 for just a seven-count pack). Clearly, these are premium-priced products—makes sense for a brand that was previously only sold at Sephora, Ulta Beauty, Erewhon, and Sprouts.

If you read our magnesium deep dive, you know this is a calculated bet. Moon Juice founder Amanda Chantal Bacon essentially created the cultural conditions for magnesium to go mainstream. When Magnesi-Om launched in 2023, magnesium was still a niche wellness obsession. Then the “sleepy girl mocktail” exploded on TikTok, Moon Juice’s pink powder became the star ingredient, and suddenly everyone was convinced they were deficient. The supplement went from Erewhon checkout line to For You Page in about six months.

… which brings us to an interesting tension: Moon Juice always had this air of elitism and exclusivity. To see it grace the shelves of Target is… unexpected. But at the same time, Target is doing a great job of positioning itself as a wellness destination. And Moon Juice’s successful Ulta launch offers a telling preview: it outperformed Sephora—a clearly prestige-focused retailer.

Given that $55M+ has poured into the magnesium beverage category alone in the past year, the VC world agrees that magnesium is the new “it girl” of wellness. But will a $44 jar of powder take off at Target… or just collect (moon) dust?

Squeeze bottle supremacy. Soom Foods (my favorite tahini!! - Jenna) is introducing its new flavored tahini squeeze bottles—in Everyday, Mediterranean Herb, and Harissa (YUM?!). The launch aims to elevate tahini from a specialty ingredient to a staple in everyday cooking, appealing to a growing demand for convenience and global flavors.

Another strategic slashes assets. Nestlé is offloading its remaining ice cream assets (including Häagen-Dazs and Drumstick) to Froneri for about $1.3 billion, marking a strategic move as CEO Philipp Navratil labels the segment “a distraction.” This decision follows a broader initiative to streamline operations, with the company also eyeing exits from vitamins and water businesses (which includes Sanpellegrino and Perrier).

The big guys want out of ice cream. At the end of last year, Unilever also spun out its ice cream business to focus efforts elsewhere.

More proof that dairy is back. Nurri, the high-protein ultra-filtered milkshake brand, just dropped something new—and it’s not another can. They’ve launched a 64oz carton of lactose-free protein milk, packing 20g of protein per serving.

Nurri is betting, loudly, that the ultra-filtered dairy category has room to grow well beyond the shakes aisle. Just last week, the brand rolled out high-protein dairy coffee creamers exclusively at Walmart. It’s very clear they want to become a fridge dairy staple.

This is more dairy validation. Not raw milk, but ultra-filtered, lactose-free, high protein, lower sugar milk. And if the growth of Fairlife, Nurri, and Slate Milk is any indication, consumers want those good macros (without the tummy aches).

This dairy resurgence isn’t happening in a vacuum. Add it to the growing list of dairy brands absolutely crushing it by leaning into real protein—Sourmilk, Painterland Sisters, Alec’s Ice Cream—consumers are returning to dairy, but seeking upgraded versions.

Speaking of dairy… BabyBel launched BabyBel Pro, a take on their iconic cheeses with 5g of protein and 1 billion live prebiotics per cheese. Because when all your brand friends are launching gut-healthy, protein-amped versions of whatever they offer, you jump off that bridge, too.

This is just 1g more of protein than their regular cheeses, which already have 4g—not really a meaningful leap forward here. It’s another example of a big strategic brand hopping on a marketing trend, but simply missing the mark at the product level.

Retail

Walmart’s grocery grip tightens. Walmart’s grocery penetration has hit a record 72%—up 6 percentage points year-over-year—as price sensitivity pushes shoppers toward lower prices. Meanwhile, mass-channel retailers (stores where grocery is one department among many—think Target, Walmart) have matched traditional supermarkets (ex. Kroger, Safeway, Publix) at 79% penetration, a first.

“Penetration” here means the share of US households that shopped a given retailer for groceries at least once over the past year.

Traditional supermarkets used to have a meaningful household reach advantage. The fact that mass retailers have closed that gap—and Walmart specifically is up 6 points in a single year—tells us a few things. For one, it signals that price pressure is pushing shoppers to consolidate trips at wherever they perceive the best value. At the same time, there are other factors at play: stores like Target and Walmart have seriously improved their grocery selections (especially pouring into the wellness category), and shoppers are looking for increased convenience—which a one-stop shop clearly provides.

Funding news

Your loss, Coca-Cola. Just Ice Tea—the organic, fair trade, less-sweet iced tea brand—just secured a $9 million Series B funding round. With sales projected to hit $30M this year, the brand is doubling its retail presence to 12,000 stores—and this latest infusion of cash could bolster its distribution and product development efforts.

Some context: Just Ice Tea is the brainchild of Seth Goldman, co-founder of Honest Tea, which was acquired by Coca-Cola… and then brutally discontinued. Three years after Coca-Cola stopped production of Honest Tea, Goldman took matters into his own hands and founded a new iced tea brand with the same mission and values.

Changing the RTD coffee landscape. Throne SPORT COFFEE, a “charged” ready-to-drink coffee brand (boosted with vitamins, electrolytes, and amino acids) secured a $10 million Series A funding round. The brand also announced its partnership with Big Geyser for direct store distribution (DSD) in the NYC metro area. The brand is current sold in 7,000 retail doors nationwide, with plans to scale to over 20,000 by the end of this year.

This raise makes a lot more sense when you look at who’s behind it. Michael Fedele, founder of SPORT COFFEE knows a thing or two about scaling a sports-adjacent beverage brand: He ran marketing at BODYARMOR from roughly $1 million in retail sales to over $1 billion before its eventual acquisition by Coca-Cola for nearly $6 billion. He was instrumental in negotiating dozens of partnership deals with high-profile athletes. So, when starting SPORT COFFEE, it only made sense to join forces with the one and only Patrick Mahomes.

RTD coffee has been in a weird quiet stretch. A few years ago, it felt like everybody had a can—but then shelves got crowded, and a lot of brands either stalled out or disappeared. Throne feels like part of the next wave of entrants taking a cleaner shot at the category with more more functional positioning, tighter branding, and stronger distribution plans. Alongside Sport Coffee there are some new brands making waves like Laurel’s, Happy, Nguyen, and Bee Keepers.

There’s no denying energy has eaten into coffee’s territory. Energy brands have had more room to play with bold claims, louder flavors, and constant innovation. And as Mark Gallo, a seasoned beverage expert, shared with us: the real opportunity may be on the distributor side. Legacy energy moves massive volume, but it doesn’t always give distributors fresh stories to sell. A “charged” coffee that can sit between RTD coffee and energy could be exactly the kind of incremental innovation they’re looking for.

Spare your eyes, listen to us yap.

Check out our recent episode of The Curious Consumer!

If you haven’t yet, please subscribe, like, leave a comment, and share it! It helps us continue to bring you the most interesting news + nuance in consumer and retail every week.

So much good stuff to unpack here but I will say … I’m not that keen on protein Doritos… respectfully ew? 🤷🏼♀️

🤩