The State of Beauty & Wellness

How beauty & wellness retailers are navigating consumers who want both efficacy and simplicity

Beauty and wellness is one of the most active—and most crowded—spaces in consumer right now. The shelves are fuller, the claims are louder, and retail buyers at every level are spending real time hunting for products that feel differentiated and easy to explain to a customer who’s already overwhelmed.

For this report, we partnered with Faire—the world’s largest online wholesale platform connecting hundreds of thousands of brands and independent retailers. If you’ve ever walked into a cute boutique and wondered how they find their products, chances are, it’s Faire.

Independent retail is a corner of the market we don’t often get clean data on, and that’s exactly what makes this interesting: Faire sits in the middle of millions of transactions across both sides of the marketplace, giving a grounded, real-world read on what’s gaining traction before it becomes consensus.

We cover the bigger retail picture every week in Express Checkout—what’s moving at Target, what’s landing at Ulta, what’s driving mass market momentum. But independent retail is where trends often incubate before they scale. These buyers move faster, take more risks, and aren’t locked into quarterly category reviews. What’s resonating at boutiques and gift shops today tends to show up in major retail assortments tomorrow.

The Faire data isn’t just a window into indie retail—but a preview of where beauty and wellness is heading at every level.

One theme runs through all of it: science-backed, lab-derived ingredients and “clean,” natural, free-from claims are trending at the same time. By the end of this, you’ll have a framework for making sense of what consumers actually want (even when they seem to be asking for contradictory things), what retailers are betting on, and where the real white space is.

Let’s get into it →

Section 1: The State of Beauty & Wellness on Faire

From Q3 to Q4 2025, Faire’s Beauty & Wellness ecosystem expanded across every dimension that matters:

Beauty and wellness is one of the fastest-growing spaces in consumer. Both prestige and mass beauty retail dollar sales grew by around 4% and 5% respectively in 2025. Increasingly though, beauty and wellness are converging into one category.

At the retail level, the lines have dissolved quickly as retailers like Ulta have expanded its in-store Wellness Shop to 30–45 feet across hundreds of stores, adding supplements and recovery brands alongside skincare and makeup.

Target added 2,000+ wellness items in a single January refresh and has been steadily expanding its beauty footprint adding nearly 3,000 brands.

The categories are converging on the shelf, and retailers are leaning into it hard.

Retailers who still think in traditional beauty vs. wellness silos are already behind. Consumers are changing how they think about taking care of themselves, which means brands need to change their framing:

The brands winning right now aren’t asking “are we a beauty brand or a wellness brand?”

They’re asking “what does our customer’s morning routine look like, and how do we fit into it?” That’s a fundamentally different question, and it leads to fundamentally different products, packaging, and retail placement.

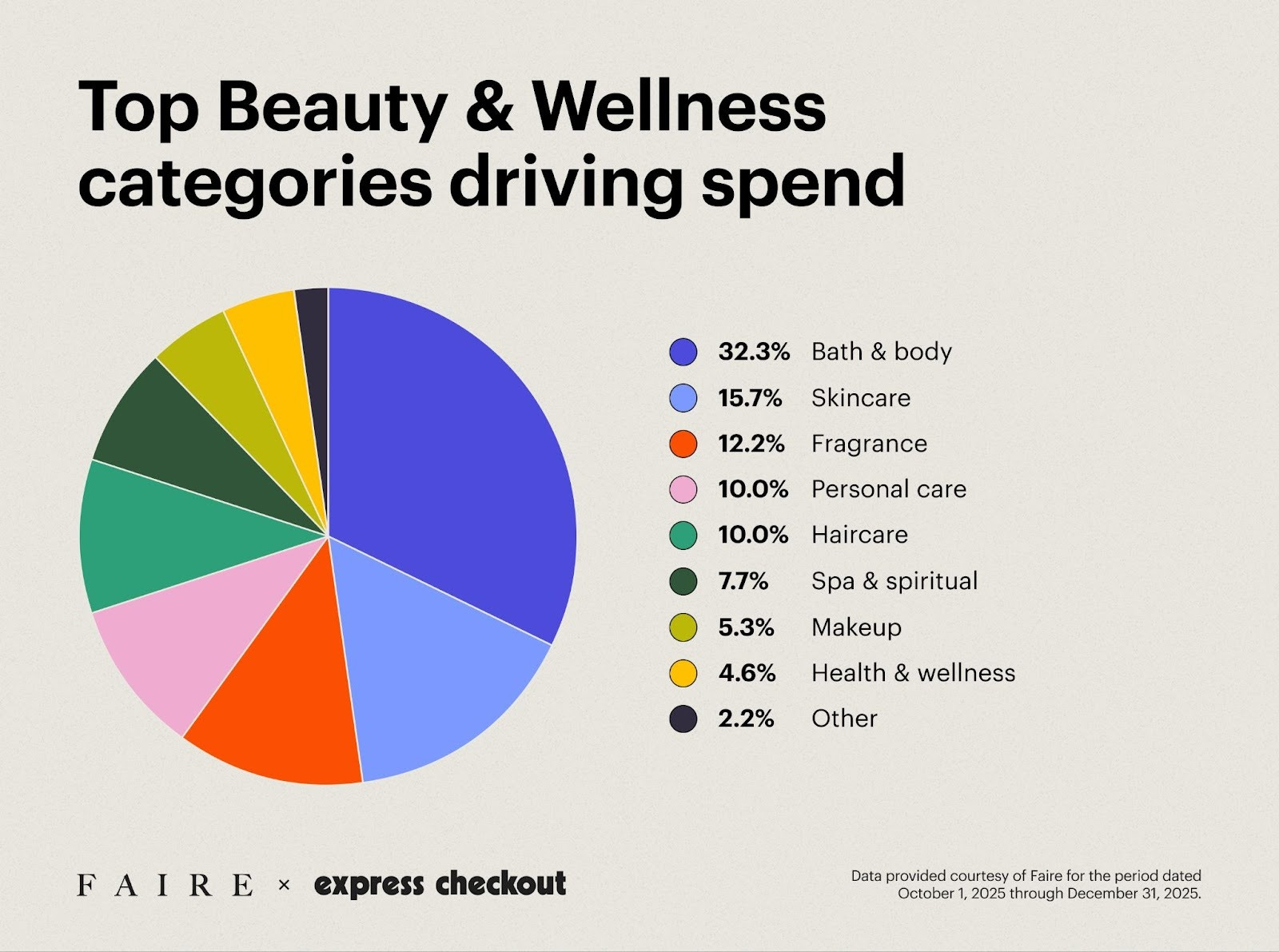

Where the spend is actually going

Body care was the highest grossing beauty and wellness category on Faire in Q4 of 2025. This category is having a real moment, and we think two main forces are driving it:

‘Skinification’ of body care. Consumers now expect the same high-performance actives they get from facial skincare—hyaluronic acid, peptides, ceramides—to show up from head to toe.

We’ve seen it in multiple recent launches: Tower 28’s body wash formulated for eczema-prone skin; Jones Road dropped a five-product ceramide body line; Fenty Skin entered the category; and even Olly—a gummy supplement brand—launched “vitamin-infused” body washes and serums with functional ingredients.

The “ritual” of body care. A shower used to be a shower. Post-pandemic, it’s even more of a ritual—a moment to decompress and beautify yourself, not just clean up (see the social media trend: the “everything” shower). Body care became the physical expression of the broader wellness shift: something to be “routineified” and luxuriated in—not just a daily chore.

Investors are paying attention: Hanni raised $2M to build out its Sephora business; Uni secured backing from L’Oréal’s venture arm and entered Ulta; OSEA Malibu received investment from General Atlantic.

And on the M&A side, Naturium was acquired by e.l.f. Beauty for $355M, and Dr. Squatch was scooped up by Unilever for $1.5B.

Who’s actually buying

The retailers shopping Beauty & Wellness on Faire are more diverse than you might expect, featuring gift shops, spas and salons, and clothing boutiques. Traditional beauty-focused retailers make up less than 5% of the mix.

In other words, the shelf context has changed. These buyers are looking for products that fit into a broader lifestyle edit, not just a skincare routine. Products that tell a quick, clear story and merchandise easily alongside non-beauty items.

There’s a cultural element driving this: Beauty routines have become more public. Rhode built a phone case specifically designed to hold its Peptide Lip Treatment. Starface turned pimple patches into something people wear proudly on their faces in public, on camera, out at dinner.

Products and routines have become identity markers and conversation starters—and as a result, the line between “beauty product” and “lifestyle product” has started to disappear.

Section 2: The ingredient split: Science vs. Clean

What the trending ingredients actually show

Looking at growth ratios for ingredients on Faire, a pattern emerges. Some of the fastest-growing items are unambiguously science-forward:

Hydrocolloid: the ingredient behind pimple patches; mechanism-forward, clinical-sounding, but the format has become approachable through brands like Starface

Oxybenzone: a synthetic UV filter found in chemical sunscreens; once controversial in clean beauty circles, now growing

Cica (Centella Asiatica): straddles both worlds; it’s a plant extract, but associated with K-beauty’s clinical skin-barrier science

Lysine: an amino acid, increasingly showing up in hair and skin formulations with a clinical positioning

Glycerin: one of the most established, well-researched humectants in skincare; it’s the quiet workhorse of moisturizers

Peptides: firmly in the “clinically proven” camp

But ‘clean’ ingredients and claims are growing right alongside them:

Rosehip: a botanical with a devoted following; positioned as a natural alternative to synthetic retinoids

Clean (as a tag): the single most tagged attribute in the dataset

Allergen-free (as a tag): formulated without common irritants or sensitizers; increasingly a baseline expectation rather than a differentiator

Shea: a plant-derived butter long used in moisturizers; beloved in clean beauty for its rich, skin-barrier-supporting properties

Aloe: the original “natural” skincare ingredient; soothing, hydrating, and one of the most universally recognized clean beauty staples

Turmeric: A classic clean beauty hero ingredient, now showing up in skincare as well as supplements

Vegan (as a tag): free from animal-derived ingredients; increasingly table stakes for brands positioning in the clean space

And then there’s bakuchiol, which is an especially interesting ingredient.

Bakuchiol is a plant-derived compound that’s functionally positioned as a “natural retinol alternative”—and it’s growing at 2.1x.

The reason it’s fascinating: it literally lives on the line between the two camps. It has an active, clinical mechanism (comparable retinoid-like effects) but comes from a plant source and is marketed under the clean beauty umbrella. Consumers who are afraid of “retinol” (too chemical, too harsh) can embrace bakuchiol. It’s the same result in a more approachable story.

Beekman 1802 is a great example of a brand doing this well. One of their best-selling products is a Bakuchiol serum—science-forward in mechanism, clean-forward in positioning. They’ve built their entire brand identity around living in the middle ground between science-backed and clean… and they are executing on it well.

What’s the actual difference?

The ingredient conversation in beauty & wellness often gets framed as a battle of natural vs. chemical and science-backed vs clean.

In practice, it’s kind of a war of vibes.

“Clean” is shorthand for natural, simple, and “free-from.” It is often built around hazard thinking. So if an ingredient could be harmful in any amount, it gets put on an exclusion list.

“Science-backed” is shorthand for clinical, lab-derived, active-driven. Formulation tends to use synthetic and natural inputs based on performance and testability.

Where this gets messy is that “clean” is often used to vilify “science.” That is chemophobia at work, and it’s sticky. Dermatology and medical voices have cautioned that “natural” and “clean” are not synonyms for safe, and that the clean beauty movement can increase confusion for consumers (including around hazard vs. real-world exposure).

But the truth is that dose matters. Formulation context matters. A product can be aggressively science-y while still being gentle, and a product can be natural while still being irritating.

At the same time, clean beauty is a real commercial success, and consumers demand it, even when the definitions are inconsistent across retailers and brands.

Some brands are actively fighting this. Experiment (started by two chemists) and Prequel (started by a dermatologist) are two doing it especially well—leaning hard into transparency and education rather than defensiveness, making the science feel like a feature rather than a disclaimer.

What they share: they don’t treat the consumer as someone who needs to be convinced of chemistry. They treat them as someone who is curious and wants to understand.

We love Experiment’s recent Sephora launch as proof that the pendulum is swinging back.

But the data is clear: brands are winning on both sides. Looking at the fastest-growing brands on Faire, a few patterns emerge across the rising names:

Ginger Lily Tallow (16x growth) is about as clean and ancestral as it gets—tallow-based skincare that trades on the back-to-basics, free-from-everything ethos.

The Outset (4.3x growth) sits firmly in the science-meets-clean sweet spot—clinically studied minimalist skincare with an emphasis on barrier function.

Avocado Zinc (one of the top-reordered brands) merges the natural (avocado oil) and the clinical (zinc) in its very name—and keeps getting reordered, which is the truest signal of retail success.

Our read: the future isn’t clean winning or science winning. Instead, it’s brands that can deliver clinical results in an approachable story—bakuchiol instead of retinol, hydrocolloid patches instead of “salicylic acid spot treatment,” barrier-focused instead of “synthetic ceramide complex.” Same mechanism, but with a clearer narrative focused around efficacy. That’s the playbook moving forward.

Section 3: What retailers are betting on

Retail assortment is a bet on the future. The tags, claims, and ingredients retailers prioritize reveal what they believe shoppers will reward—and right now, two bets are running in parallel.

Bet 1: Consumers want fewer perceived irritants.

The clean, free-from, allergen-free cluster continues to grow. Cruelty-free is up 1.5x. Paraben-free up 1.3x. Vegan up 1.4x. “Clean” as a product tag appears on more than 17,000 products and is still climbing. For brands, the implication is straightforward: these claims are increasingly table stakes, not differentiators. Having them won’t win you the shelf. Not having them might cost you it.

One callout worth making: “silicone-free” (0.92x) and “tallow” (0.34x) are actually underperforming average growth—which tells us that hyper-specific free-from claims and niche ancestral ingredients are still culturally loud but commercially quiet. TikTok beef tallow discourse doesn’t equal Faire wholesale demand. Trend awareness and purchasing behavior are two different things, and indie retail buyers are closer to the latter.

Bet 2: Consumers still want performance—especially at accessible prices.

Active ingredients with legible mechanisms are winning. Hydrocolloid’s 6.2x growth is the clearest example: the patch format makes the product’s function completely visible. You put it on, you see the gunk, the product worked. No chemistry degree required. AHA (1.5x), retinol (1.4x), salicylic acid (1.3x), niacinamide (1.1x), glycolic acid (1.1x)—all growing alongside clean claims, not instead of them.

The throughline for brands: science wins when it’s explainable in a sentence. If your product’s clinical story requires a paragraph, it will lose to a simpler “natural, clean” narrative almost every time at the indie retail level. Lead with the outcome, not the mechanism.

On price: 80%+ of Beauty & Wellness GMV on Faire sits below $25, which tracks with what Circana is seeing across the broader US market—mass beauty is gaining momentum on prestige. But budget doesn’t mean commodity. The products generating high reorder rates—Wild Botanicals, HiBAR, Ursa Major, Little Seed Farm—carry a value signal or ingredient story that justifies the purchase beyond price point. That’s the sub-$25 sweet spot: something that performs and, at the same time, gives the customer something to tell their friend about.

The retailers winning in beauty right now aren’t choosing between clean and science—they’re merchandising both, clearly, and letting customers self-select. For brands trying to break into this channel, the question to answer is simple: which story are you, and can a buyer explain it in thirty seconds to a customer who’s never heard of you?

⬇️ Explore Faire’s Beauty & Wellness category ⬇️

Section 4: Methodology & notes

All percentage figures in this report are share-based, not raw GMV dollar amounts—Faire’s data is presented as proportional breakouts to protect individual brand and retailer privacy. Growth ratios for ingredients represent the relative change in products tagged with that ingredient on Faire, not broader market search or sales data.

A few important caveats:

Tag data reflects how brands choose to describe their products—which is itself a marketing signal, not necessarily a formulation audit

Newer tags may show inflated growth ratios due to low absolute baselines

Category definitions are Faire’s internal subcategory taxonomy and may not map 1:1 to how other industry reports define the same segments

State-level retailer data reflects proportional retailer distribution, with California (9.3%), Texas (7.3%), and New York (4.9%) as the top three markets