Everything is Erewhon now.

Plus: More celebrity beverages, branded peptides, a shot for sleep and more...

Hello hello!

We’ve said it before, we’ll say it again (even in this very edition): Walmart is becoming the destination for fast-growing CPG brands.

That first confirmed Walmart PO is a BIG deal! But at the same time... it’s also not cash.

Behind that massive W is a pile of costs: production, supplier deposits, inventory—all due before Walmart pays on net terms. That gap between “we got the PO” and “Walmart actually pays us” is where a lot of otherwise-healthy suppliers get squeezed.

That’s why we’re excited to share Bridge—the direct lender behind Walmart’s official PO Financing Program. They fund up to 100% of COGS on approved Walmart and Sam’s Club transactions (loan sizes up to $10M), and handle everything from underwriting through repayment—no brokers needed.

If you just landed a Walmart order—or you’re close—you’re going to want Bridge in your corner.

Get instant cash on your Walmart PO

News of the Week

Everything is Erewhon now.

In the past few weeks, two more stores joined the cult. Laurel Supply opened May 8 in West Hollywood—blond wood, a sushi counter, $16 smoothies, and a location roughly a block from an Erewhon.

A week later, Nude Miami opened in Brickell confidently calling itself “the healthiest grocery store in America,” seed-oil-free, with a literal bouncer at the door. Add NYC’s latest bougie grocers, Meadow Lane and Happier Grocery, and there’s a clear trend happening here.

Erewhon created a category, and now everyone wants in.

The playbook is, by this point, fully copy-pasteable:

A ridiculously photogenic organic produce section

A seed-oil-free hot bar/prepared food section

Supplement-stacked, marbled smoothies

“Clean” trendy snacks (featuring $15+ Masa Chips, without fail)

A premium wellness section stocked with sea moss gels and “clean” face wash

We already know why this works, and a big piece of it is accessible luxury. A $20 smoothie is a lot for a smoothie, but there’s no waitlist and no $1,000 price tag. For the cost of a slop bowl lunch, you get to feel elevated, in-the-know, a little bougie… and then you get to post it, AKA turn it into social capital. Groceries became the rare status object that’s both attainable and instantly shareable. In High Snobiety’s recent survey on wellness, 74% of respondents said that wellness products signal they’re “dialed in.”

In other words, food/bev/wellness is identity now, and these stores sell identity by the basket (carts are for plebs). But that’s exactly the point: these aren’t really grocery stores.

Though this is largely anecdotal (Erewhon doesn’t reveal much data about its shoppers), the dominant Erewhon behavior isn’t the full weekly shop—it’s the occasion visit, the smoothie run, the “I can only get this here” discovery peruse and pickup. Full-basket grocery shopping at one of these places is almost anthropologically rare (and nearly physically impossible by design… have you seen the width of their aisles?!).

The product, then, is discovery—a shortcut for people who want to optimize cart curation without reading forty ingredient labels. You don’t go to Erewhon to stock a pantry; you go to find what’s next, and to be seen finding it.

For a while, that frontier was theirs alone. The thing is, now mass-market retailers like Target and Walmart are trying their hand at the discovery play:

Target rolled out 2,000-plus new wellness items this year—600 exclusives, over half under $10—framed, explicitly, around helping shoppers “discover new categories.” Food and beverage is now Target’s No. 1 traffic driver, and it’s leaning into “merchandising authority” with nearly 50% more newness, more emerging brands, and an expanded wellness push: protein-forward items, organics, better-for-you swaps next to the owned brands shoppers already know.

And if you’re on the same side of IG as we are, you’ve probably seen one of the dozens of videos claiming Target is the “new Whole Foods.”

Walmart built a modern-soda set around Poppi, Olipop and Culture Pop, launched a better-for-you private label (bettergoods), and is pulling synthetic dyes and 30-plus additives from every private brand it owns by 2027, one of the largest reformulations in retail history.

The discovery formula and ingredient bans that once made the Erewhons of the world feel exclusive could (slowly) become table stakes at the country’s biggest retailers. Isn’t that a threat to the new designer-smoothie-purveyors on the block?

Ironically, we think that the deeper mass-market retailers wade into clean labels and emerging brands, the more these boutiques can justify their existence. Because the moment the soda you “discovered” last year lands in a suburban Target, it isn’t first anymore.

First has to keep meaning something earlier, weirder, more exclusive. It has to mean stumbling upon a product at the only place confident enough to call itself “America’s healthiest grocery store”—a claim that, no matter how many better-for-you brands enter its assortment, Walmart could never make.

Everything is Erewhon now—so what does that leave Erewhon (and its copycats)? Further out, more curated, more exclusive, more aggressively first. There will always have to be a room that feels more exclusive than the one you’re standing in, and always a consumer with the capital (and the appetite) to get inside it.

CPG & Consumer Goods

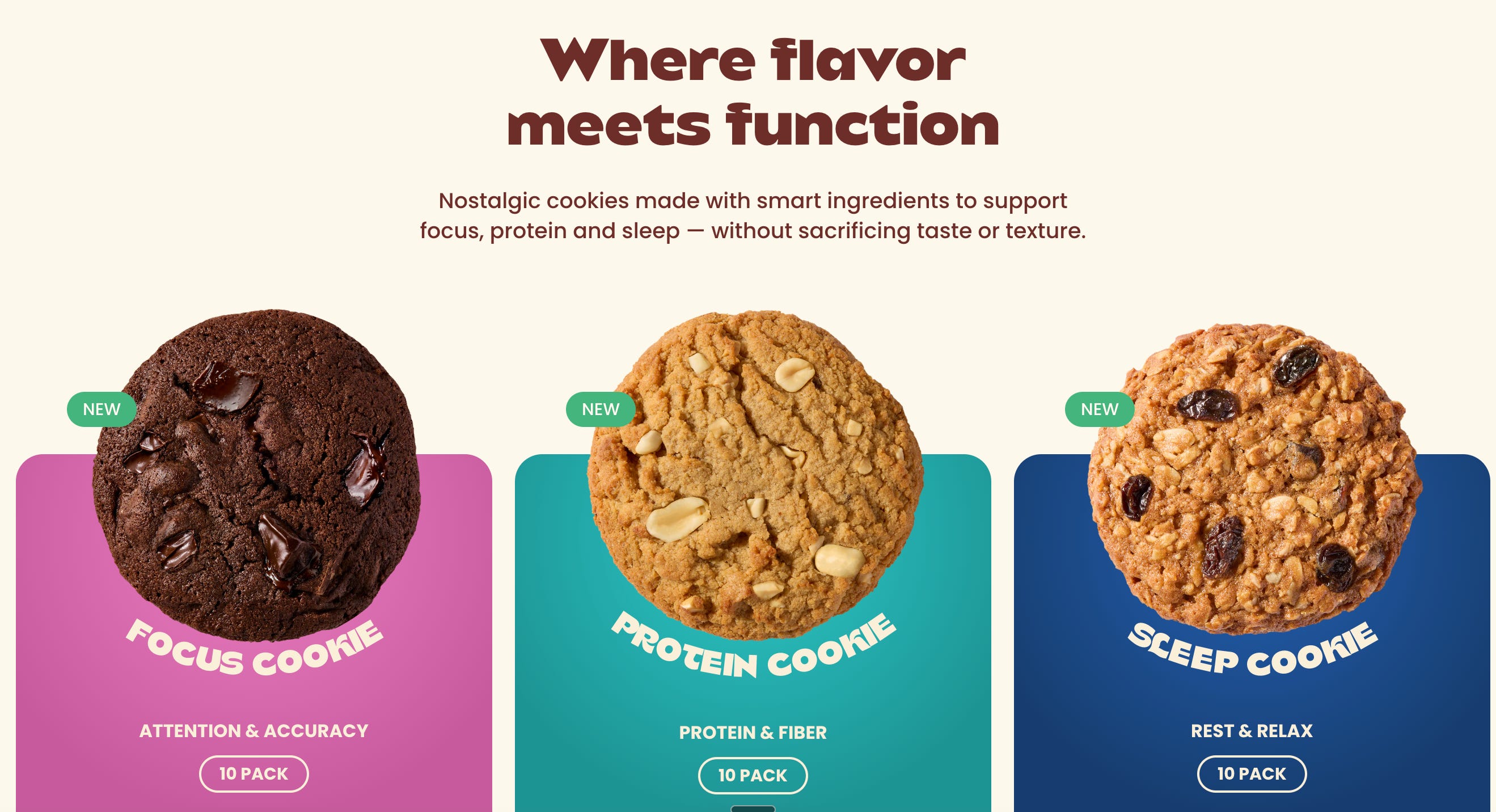

It runs in the family. Ashley Fields (daughter of Mrs. Fields Cookies founder Debbi Fields) and Kim Anderson launched Fields Good, a line of functional soft-baked cookies for focus (ft. creatine and Cognizin citicoline), sleep (ft. L-theanine), and protein (because, what else?). The brand raised a $1.8M pre-seed led by Female Founders Fund to scale DTC, expand to TikTok Shop/Amazon, and pursue retail distribution.

The Mrs. Fields heritage is doing real work here, even if implicitly. It gives the brand instant permission to be in the cookie space in a way that most functional snack startups don’t have, and validates the most important decision-maker in food—taste—before trial. At the same time, it’s setting up the brand with big shoes to fill: consumers typically have lower expectations for the taste of a functional treat than its function-free counterpart. But here, if the cookies don’t match the indulgent memory of an OG Mrs. Fields, the brand will have a lot more apologizing to do.

Separately: the irony that Mrs. Fields—whose entire empire was built on the most unapologetically indulgent cookies imaginable—now has a legacy brand in the “functional soft-baked cookie” space is…. funny.

She sure loves an exclamation point. Supergoop! founder Holly Thaggard and her son Will launched WaterOuai! They’ll be sourcing water from Texas’s Edwards Aquifer and packaging it in the SUPERCAN, an innovative aluminum can designed to avoid BPA/PFAs/phthalates and reduce material transfer.

This feels part of a larger movement towards the new era of water bottles. WaterOuai isn’t alone in betting on microplastics fear seeping into our water bottle usage: Loonen, the new status-symbol water founded by venture investor Clara Sieg, launched late last year with exhaustively tested, PFAS-free spring water in glass bottles, arguing that “the organic movement never came for water, because it’s not grown.”

WaterOuai is launching DTC and on Amazon at $2/can or $48/case, with an initial distribution focus on schools, universities, corporate offices, and boutique hotels—the same institution-first strategy Thaggard used to scale Supergoop!

Say it with me folks….”Another! Celeb! Protein! Product!!” Kristin Cavallari—reality TV alum (Laguna Beach / The Hills) and founder of Uncommon James—is launching Fizzen, a sparkling juice with protein, collagen peptides, and B vitamins.

Sell the uppers and the downers. Magic Mind, makers of a line of mental performance shots, launched a new drug-free 2 oz sleep shot. The shots include ingredients like lavender, L-theanine, Magnesium Glycinate, and plant-based melatonin. The shot is available online and is launching this month in Sprouts, HEB, New Seasons, and Central Market.

Magic Mind owned your mornings—now it wants your nights. The brand made its name selling 2 oz “mental performance shots,” a mixture of caffeine and nootropics to get you through the day, that it’s sold since 2020. Now with a sleep shot, Magic Mind can bookend your whole day. A shot to wake you up and a shot to put you down. Is it mind control or just clever positioning? Either way, owning both ends of your routine is a smart way to double the number of times a day you reach for the same brand. I’m just glad it’s not another gummy.

And let’s not forget, sleep is big business. The global sleep economy was valued at roughly $616 billion in 2025 and is still climbing—smart mattresses, trackers, magnesium gummies, mouth tape, and now microdosed sleep shots. Magic Mind is wedging into a category where consumers have already proven they’ll spend whatever it takes to chase a better night.

Surprise, surprise, another functional drink. YouTuber and makeup artist Tati Westbrook launched Unfair Advantage, a functional powdered energy drink with 75mg natural caffeine from guarana, prebiotics, and, of course, skin-support claims.

It looks like you told AI to make you a functional powdered drink brand…

Cereal wants its health halo back. WK Kellogg rolled out SPOONS, an on-pack nutrition framework (simple ingredients, protein, outstanding fiber, other nutritious foods, nutrients you need, single-digit sugars) across Corn Flakes, Raisin Bran, and Rice Krispies. This is the first notable move under its new owner Ferrero.

SPOONS is a proprietary label that Kellogg’s designed itself, so it can highlight whatever it wants—it’s not a third-party standard. The FDA has been pushing for front-of-pack labeling for exactly this reason, but brands keep beating regulators to the punch with their own friendlier-looking versions.

Target’s keeps recruiting chefs. Target’s in-house brand Good & Gather launched a limited-edition snack line with James Beard Award-winning chef Roy Choi. They’re dropping new sweet and savory snack items such as Spicy Ramen Yuca Chips, Wassapi Ranch Popcorn, Chili Lime Cake Pops (confused about this one tbh), and more across nearly 1,800 stores starting May 31, all under $6.

This isn’t the first time Target worked with chefs on its in-house brands. Good & Gather Collabs launched in 2025 with James Beard chef Ann Kim on frozen pizza, then pitmaster Rodney Scott on barbecue, and now Roy Choi on snacks. They’re borrowing these chefs culinary credibility to elevate their own brand and keep Target a place of discovery and taste as a way to differentiate the grocery arm beyond just the branded products on the shelf.

Looking good means smelling good. Dwayne “The Rock” Johnson’s fast-growing men’s grooming line, Papatui, has expanded into cologne with three scents at about $40 each, built with perfumers Frank Voelkl (DSM-Firmenich) and Jérôme Epinette (Byredo, Sol de Janeiro), and sold at Target..

Back in October 2025 we said “Men want to smell good now” —and it couldn’t ring more true today. Men’s skincare, and fragrance especially, is one of the few corners of beauty putting up consistent wins, and it’s not slowing down. Papatui is already the #1 brand in the Men’s Skin Care category at Target (sales per IRI/Circana), so moving into cologne is a logical next step for them.

eCommerce

From retailer to AI infrastructure vendor. Amazon announced Agentic Shopping Assistant on AWS, licensing its AI shopping tech to outside retailers for deployment within 60 days—Tapestry (Coach, Kate Spade) went live first, with more retailers in testing.

In other words, Amazon is selling the AI layer that could help brands reduce their dependence on Amazon’s own marketplace—while also keeping them firmly in the AWS/Bedrock ecosystem. Freeing them from one Amazon dependency, landing them in another….

AWS specifically called out CPG brands as a use case—the argument being that no one knows their products better than the brands that make them. The pitch is that proprietary product knowledge plus proven AI infrastructure beats a generic assistant every time. Whether CPG brands have the dev resources to actually deploy this is a different question.

Retail

Calling all retail nerds! 📣 We are heading to Retail Brew’s Clicks, Bricks & Everything In-Between on June 3 at Studio Gather (45 Rock, NYC). Half-day, 8 AM–12:30 PM, all about how omnichannel is actually playing out.

We’re moderating a session called “Getting Discovered with Express Checkout” at 9:30am, where we’ll get into how consumer brands are creating demand in a fragmented landscape with Little Spoon’s Caryn Wasser.

Funding

Betting peptides go legit. Feel Peptides closed a $3 million seed round led by Sugar Capital—investors in brands like Caraway, Starface, and Grüns (acq. Unilever 2026)—to bring trust and better branding to the growing peptide market.

Peptides are the latest thing that American consumers are experimenting with to become the most productive, hot, athletic version of themselves (and also defy all laws of aging). If you’re as confused as we are about this growing market, our friend Dan Toomey made a great (hilarious) vid breaking it down.

Despite every Joe Rogan listener and their biohacking bestie promoting these products, it’s still wildly under-researched. Most peptide consumers are sourcing their vials from online sellers (often internationally) with minimal-to-no transparency on sourcing, purity, or quality. So if somebody is going to inject themselves with these products, might as well come from a brand that promotes testing, quality standards, and control—which is what Feel Peptides seems to be promising.

Stay tuned: we’ll have a longer piece on this topic soon.

OxiClean’s parent just bought a stain-remover cult. Church & Dwight acquired Miss Mouth’s Messy Eater for ~$325 million. The brand did ~$80M in net sales and ~$28M EBITDA in 2025, built almost entirely on eCommerce. It’s currently the #1 stain remover on Amazon.

Church & Dwight already owns the heavy hitters of stain removal (OxiClean, Arm & Hammer), so sure they’re buying market share but what they’re really buying is a consumer. Miss Mouth’s positions itself as natural and non-toxic while still claiming to work as well as the harsh stuff, which is exactly what shoppers now want from the products they use around their kids and kitchens. The whole household-care aisle is moving away from “chemical” and toward “clean but still effective,” and C&D just bought the brand that’s already won that argument with consumers.

Splenda just gobbled up the sweetener aisle. Heartland Food Products Group announced an agreement to acquire Whole Earth Brands’ Americas business, adding Equal, Whole Earth, Swerve, and Chuker to its Splenda, SlimFast, and Java House portfolio. Financial terms were not disclosed.

In case you didn’t know, R&B singer and actress Patti Labelle has a food brand called Patti’s Good Life which started in 2008. They reportedly do around $80M+ a year and just raised a strategic investment from Factory’s Supply Factory, Lafayette Square, and Innovate Capital to scale distribution and expand its frozen and family meals portfolio.

The frozen aisle keeps pulling in serious money. Brands have been launching and raising left and right. Frozen waffle brand Evergreen pulled in $15M, Laoban raised $7M for its frozen Asian lineup, Jesse & Ben’s closed a $10M Series A for its clean label fries, and stuffed pasta brand Ripi landed $2.4M ahead of its Target rollout. It’s no wonder this is all happening right now, U.S. frozen food sales hit $87 billion in the 52 weeks ending September 2025, up more than 45% from 2019, with frozen snacks alone up nearly 70%! It’s where shoppers are going to save money without sacrificing on quality.

Is makeup coming back? Violette_FR, a beauty brand founded my French makeup artist Violette Serrat, raised $5M from existing backers Silas Capital, Monogram Capital Partners, and Highlander Partners, extending its 2024 Series B as prestige makeup brands faces sluggish category growth and limited exit opportunities.

Prestige makeup grew just 2% in Q1, compared to 10% for prestige haircare and 7% for both skincare and fragrance—which explains why “extending an existing Series B” rather than closing a fresh round is the financing structure of the moment. Westman Atelier did the same thing earlier this year. Investors in these brands aren’t panicking; they’re holding, waiting for the category to turn. The French-girl-beauty positioning and tight SKU edit (Violette_FR has no complexion products) at least gives it a defensible identity that isn’t just trend-dependent.

The anti-Amazon is gaining steam. Stord raised $250M at a $3B valuation led by Strike Capital alongside Kleiner Perkins and Founders Fund. Stord runs warehouses and fulfillment software that let brands offer Amazon-level shipping speed without handing Amazon the customer relationship; the Atlanta company, started by two Georgia Tech students in 2015, has now raised roughly $775M in total.

Ôrebella closed a Series A led by Silas Capital and named its first CEO, Anish Agarwal (ex-T3 Micro and Colgate-Palmolive). The clean-fragrance line launched in 2024, is sold in Ulta’s worldwide and industry estimates peg 2026 revenue at $20–30M.

Call it the Wagyu of pork. Campo Grande raised $4M to bring its heritage pork brand into more retail doors across the country. Backers include Valor Equity Partners, Spacestation Investments, Supernatural Ventures, and Chomps co-founder Pete Maldonado.

ButcherBox’s retail move is a useful parallel: the DTC subscription brand made its first major retail leap in January, landing fresh grass-fed beef in over 1,400 Targets—and the bet is paying off from a position of strength, with subscription revenue already exceeding $570M in 2025. If a brand built entirely on the premise of “better meat, delivered” can successfully cross into mass retail without diluting its identity, it’s a good sign for Campo Grande’s ambitions to do the same at the shelf level with heritage pork.

The broader context: 80% of Americans report prioritizing protein intake during at least one meal a day, and shoppers increasingly favor “clean meat” attributes like grass-fed, organic, and no additives—with protein callouts on red meat packaging having doubled since 2019. Campo Grande is pitching into exactly that: the consumer who’s already reading labels closely and is willing to pay up for provenance. Heritage breed pork is a natural next frontier as beef prices stay elevated—ground beef averaged $6.69/lb in December 2025 versus $4.30/lb for pork chops—which makes a premium pork brand easier to justify on relative terms even at a higher price point than conventional pork.

If you haven’t yet, please subscribe, like, leave a comment, and share it! It helps us continue to bring you the most interesting news + nuance in consumer and retail every week.

Love the Erewhon piece and would love to see the financials from these stores. At some point, the smoothie isn't competing with other smoothies. It's competing with experiences, status, and social currency. That's what makes this trend so fascinating. My guess is it's a big trend and only a few survive. https://www.expresscheckout.co/p/everything-is-erewhon-now?utm_source=post-email-title&publication_id=4153338&post_id=200189255&utm_campaign=email-post-title&isFreemail=true&r=2cb8kw&triedRedirect=true&utm_medium=email